")

Deciding what to do with your home in retirement brings important choices, especially when you want extra financial comfort without leaving the place you love. For retired homeowners across the United Kingdom, equity release offers a way to access money tied up in your property without needing to sell or move. With clear eligibility rules and different options available, you can make sense of how equity release works and find affordable guidance for managing property transfers simply and securely.

Table of Contents

- What Is Equity Release and Who Qualifies

- Lifetime Mortgages Versus Home Reversion Plans

- How the Equity Release Process Works

- Legal Protections and Adviser Requirements

- Costs, Risks, Inheritance and Family Impact

Key Takeaways

| Point | Details |

|---|---|

| Equity Release Eligibility | Homeowners aged 55 and over can access equity release, primarily through lifetime mortgages or home reversion plans, with certain property value and residency requirements. |

| Lifetime Mortgages vs Home Reversion | Lifetime mortgages allow full ownership while borrowing against property value, whereas home reversion involves selling part of the property for funds, impacting future inheritance. |

| Risks and Costs | Important costs, including compound interest and fees, can significantly impact both homeowners’ net funds and heirs’ inheritance, necessitating careful consideration before committing. |

| Professional Advice Importance | Consulting an independent financial advisor is crucial to understanding the long-term implications and ensuring informed decisions regarding equity release options. |

What Is Equity Release and Who Qualifies

Equity release represents a financial strategy designed specifically for homeowners aged 55 and over who want to unlock the monetary value trapped within their property without needing to sell or move. Equity release provides a flexible method for accessing funds tied up in home ownership, offering retirees financial breathing room during their later years.

Two primary types of equity release exist: lifetime mortgages and home reversion plans. A lifetime mortgage allows homeowners to borrow against their property’s value while retaining full ownership, with interest accumulating over time. Home reversion plans involve selling a portion or all of your property to a provider in exchange for a lump sum or regular income, while continuing to live in the home. Crucially, both options have specific eligibility requirements that potential applicants must meet.

To qualify for equity release, homeowners typically need to satisfy several key criteria. These include being at least 55 years old, owning a property in the United Kingdom valued above a minimum threshold (usually around £70,000), and having the property serve as their primary residence. Home condition and property type also impact eligibility, with providers assessing factors like property maintenance, construction, and location before approving an application.

Pro tip: Before pursuing equity release, consult an independent financial advisor who specialises in retirement planning to understand the full long-term implications for your personal financial situation.

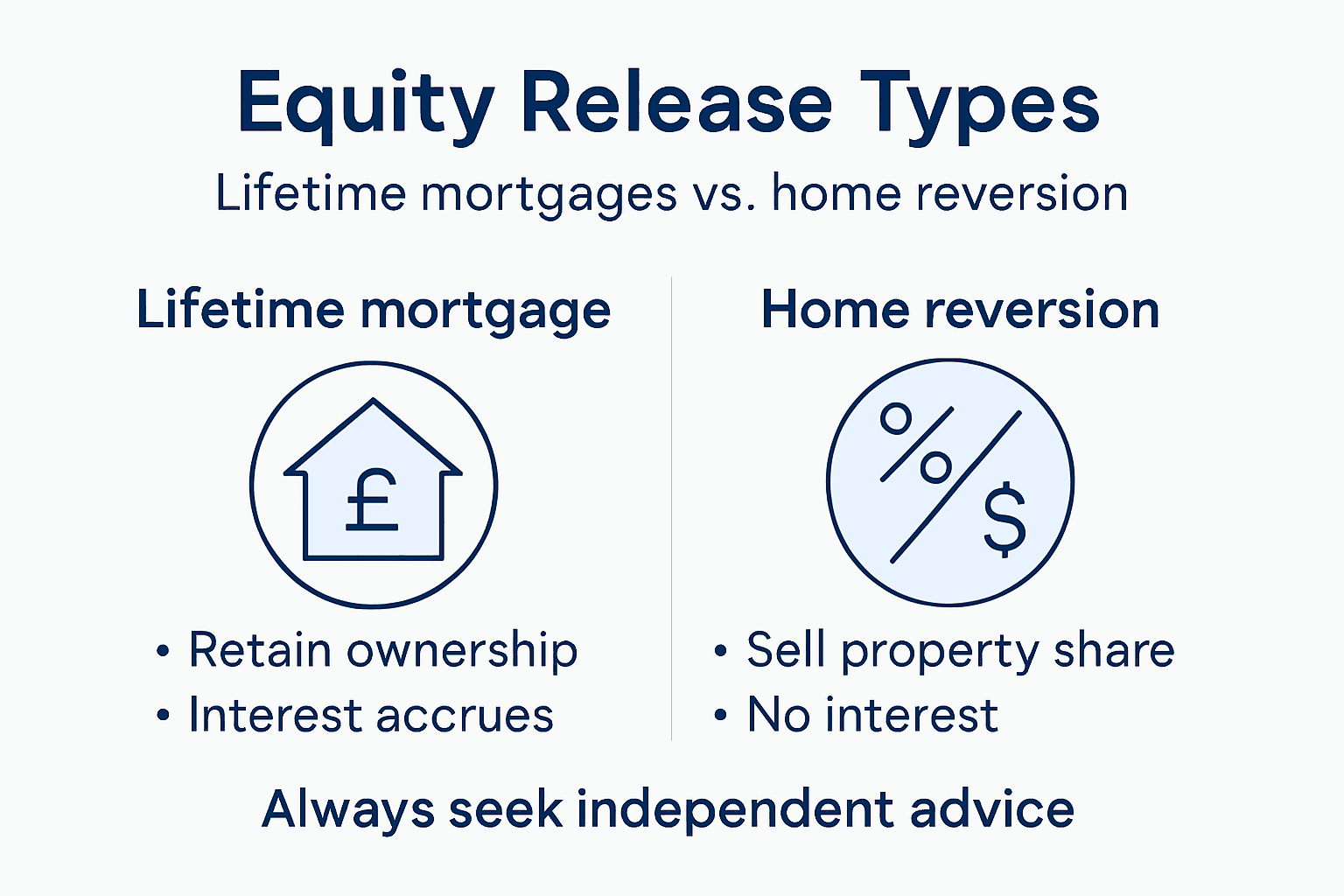

Lifetime Mortgages Versus Home Reversion Plans

Lifetime mortgages and home reversion plans represent two distinct approaches to equity release, each offering unique financial opportunities for retired homeowners. Lifetime mortgage options provide flexibility for accessing property value while maintaining home ownership, with borrowers able to access funds without immediately surrendering their property rights.

In a lifetime mortgage, homeowners can borrow against their property’s value, with interest either being added to the loan or paid monthly. The critical advantage is retaining full property ownership, and the no-negative-equity guarantee ensures you won’t owe more than your home’s ultimate value. Typically, these plans allow you to withdraw funds as a lump sum or through flexible drawdown arrangements, giving you greater control over your financial strategy.

Conversely, home reversion plans involve selling a portion of your property to a provider in exchange for a lump sum or regular income. While you can continue living in your home rent-free, the provider receives a predetermined share of the property’s future sale proceeds. These plans are generally available to homeowners over 60 and often provide lower than market value compensation, with additional costs including legal and valuation fees.

Pro tip: Always consult an independent financial advisor who specialises in equity release to understand the long-term financial implications and compare different providers’ specific terms and conditions.

Here’s a concise comparison of lifetime mortgages and home reversion plans:

| Feature | Lifetime Mortgage | Home Reversion Plan |

|---|---|---|

| Ownership | Remain full owner | Sell part or all of property |

| Minimum Age Requirement | From 55 years old | Usually from 60 years old |

| Payment Received | Lump sum or drawdown | Lump sum or regular income |

| Value Received | Usually based on market value | Often below market value |

| Repayment Timing | Upon death or care entry | Provider receives share at sale |

| Living in Property | Remain until death or moving | Continue living rent-free |

| Interest Accumulation | Compounded until repayment | No interest, provider shares value |

How the Equity Release Process Works

The equity release process involves several crucial steps designed to help homeowners aged 55 and over access the financial value locked within their property. Equity release requires careful consideration of individual circumstances, with most plans falling into two primary categories: lifetime mortgages and home reversion schemes.

Initially, potential applicants must undergo a comprehensive assessment to determine their eligibility. This typically involves a detailed financial consultation with a qualified equity release specialist who will evaluate factors such as property value, homeowner age, and overall financial health. Providers will conduct thorough checks to ensure the applicant understands the long-term implications, including how interest accumulates and potential impacts on inheritance and means-tested benefits.

Once approved, homeowners can choose how they receive their funds, with options ranging from a single lump sum to flexible drawdown arrangements. The repayment process occurs after death or permanent care entry, when the property is typically sold to settle the outstanding loan and accumulated interest. Importantly, most modern equity release plans include a no-negative-equity guarantee, ensuring that borrowers or their estates will never owe more than the property’s market value.

Pro tip: Arrange an independent financial consultation and request detailed illustrations showing how the equity release might impact your long-term financial situation, including potential compound interest scenarios.

Legal Protections and Adviser Requirements

Equity release is a complex financial product that demands robust legal protections to safeguard consumers’ interests. Financial advisers must meet strict professional standards to ensure clients receive appropriate and responsible guidance throughout the equity release process. These regulatory requirements are designed to protect vulnerable homeowners from potential financial mismanagement.

All equity release advisers are required to hold an annual Statement of Professional Standing (SPS) from an accredited body, demonstrating their competence and adherence to professional standards. The Financial Conduct Authority (FCA) closely monitors these professionals, ensuring they possess appropriate qualifications and maintain ethical practices. Advisers must provide comprehensive, impartial advice tailored to each individual’s unique financial circumstances, with a legal obligation to explain the long-term implications of equity release, including potential impacts on inheritance and means-tested benefits.

The Equity Release Council provides additional consumer safeguards, enforcing a stringent code of conduct for members. Key protections include mandatory independent advice before proceeding, no-negative-equity guarantees, and the right to remain in your home for life. These organisations ensure that equity release providers maintain transparent pricing, offer clear contract terms, and prioritise the financial well-being of retired homeowners.

Pro tip: Always request to see an adviser’s FCA registration and Equity Release Council membership, and do not hesitate to verify their credentials directly with these regulatory bodies.

Costs, Risks, Inheritance and Family Impact

Equity release represents a significant financial decision with complex implications for both homeowners and their families. Potential risks require careful consideration before committing to such a substantial long-term financial arrangement. These products can substantially impact your estate’s value, potentially reducing the inheritance you may wish to leave behind.

The financial landscape of equity release involves several critical costs that can accumulate over time. Arrangement fees, legal expenses, and most significantly, compound interest can dramatically reduce the total value of your property. Disputes often emerge from misunderstood financial commitments, particularly regarding early repayment charges and the long-term impact on family wealth. Homeowners must carefully evaluate how these costs might affect their beneficiaries’ potential inheritance, as the loan and accumulated interest will be settled from the property’s eventual sale.

Families are strongly advised to engage in open discussions about equity release, considering its broader implications beyond immediate financial needs. The decision can affect means-tested benefits, future care planning, and the overall financial strategy of multiple generations. Some equity release products offer safeguards like no-negative-equity guarantees, but these do not eliminate the fundamental reduction in estate value that occurs when releasing equity.

Below is a summary of typical costs and risks associated with equity release:

| Cost or Risk | Impact on Homeowner | Impact on Family/Inheritance |

|---|---|---|

| Arrangement Fees | Reduces net received funds | Diminishes estate value |

| Legal and Valuation Fees | Adds upfront expenses | Lowers inheritance potential |

| Compound Interest | Grows total repayment over time | Depletes estate for beneficiaries |

| Early Repayment Charges | Financial penalties if repaid early | Further reduction in inheritance |

| Reduced Means-Tested Benefits | May affect certain state support | Family may lose financial advantages |

Pro tip: Arrange a comprehensive family meeting to discuss equity release, including potential long-term financial implications, and consider consulting a financial adviser who can provide neutral, detailed projections of how the decision might impact your entire family’s financial future.

Unlock Your Property’s Potential with Expert Conveyancing Support

Equity release can offer life-changing financial freedom, but it also involves complex legal steps that can impact your property and estate. Whether you choose a lifetime mortgage or a home reversion plan, understanding how conveyancing affects these transactions is essential to safeguard your interests and secure your legacy. Common concerns like repayment timing, ownership rights, and legal fees must be handled by a trusted professional to avoid costly mistakes.

Take control of your equity release journey today by connecting with vetted, SRA- or CLC-regulated conveyancing firms, offering instant fixed-fee quotes that could save you up to 75% on legal fees. Use our streamlined service to find expert conveyancers who understand the nuances of equity release transactions and can clearly explain every step of the process.

Don’t risk delays or hidden costs. Start with our instant quote page to get matched with reliable conveyancers near you. For deeper insights, explore our detailed Step-by-Step Conveyancing Process and discover how a professional solicitor can protect your property rights throughout equity release.

Take the next step now and secure peace of mind by getting your conveyancing needs sorted quickly and transparently—visit Conveyancing-Solicitor.co.uk and request your free instant quote today.

Frequently Asked Questions

What is equity release?

Equity release is a financial strategy that allows homeowners aged 55 and over to unlock cash from their property while still living in it. This can be done through lifetime mortgages or home reversion plans.

Who qualifies for equity release?

To qualify for equity release, homeowners typically need to be at least 55 years old, own a UK property valued above a minimum threshold (usually around £70,000), and use the property as their primary residence. Factors like property condition also affect eligibility.

What are the differences between lifetime mortgages and home reversion plans?

A lifetime mortgage allows homeowners to borrow against their property’s value while retaining ownership, whereas a home reversion plan involves selling a portion of the property to a provider in exchange for a lump sum or income, all while continuing to live in the home.

What are the risks associated with equity release?

The risks of equity release include compound interest reducing your estate’s value, potential impacts on inheritance, and possible effects on means-tested benefits. Costs such as arrangement and legal fees can also accumulate over time.

Recommended

- How Does Equity Release Work? A Comprehensive Guide – Conveyancing Solicitor

- How Much Equity Can I Release: A Comprehensive Guide – Conveyancing Solicitor

- How to Release Equity from Your Home: A Guide – Conveyancing Solicitor

- Equity Release: How Long Does it Take? – Conveyancing Solicitor